I spent a few days over Christmas with my brother. He is bright, has a degree in Engineering Physics, and has discussed (and understood) resource depletion with me over the years.

He said he thought peak oil was no longer an issue due to the current global oil glut and low prices. I tried to explain to him that nothing had changed but I could tell he was not convinced. If my brother feels this way I have no doubt that most other citizens also believe peak oil is a non-issue.

They are wrong. In fact really wrong. The low prices are an indicator that the end game is in sight and that we should be very concerned.

It’s difficult to explain in a few words but here is my attempt…

- Oil is non-renewable. This means the total quantity of oil is finite.

- The quantity of oil we can extract and use is dependent on the price. If the price is high we can use more technology, energy, materials, and labor to extract it.

- Consumers want to minimize their expenditures and companies want to maximize their profits. This means we always exploit the lowest cost sources first. As the low cost sources are depleted the cost of a finite resource will increase.

- We built our civilization on oil that cost about $20 per barrel and that oil is all gone. What’s left costs on average about $80 to $100 per barrel to extract.

- It is difficult, maybe impossible, for the economy to grow with oil at $80+. After paying for the energy that every product and service depends on, there is insufficient surplus left to reinvest for growth.

- The design of our debt based money system requires growth or it collapses. We kept growth going despite high oil prices by reducing the interest rate thereby making it possible for us to afford the higher cost oil by increasing our debt load. This in turn allowed high cost producers like the tar sands, shale oil, and deep water to increase production.

- This trick of using debt to create growth works well for a while but must come to an end when the total debt reaches a level that is not sustainable even with zero interest rates. We are there now.

- Because private sector debt is now saturated the global consumer is no longer able to afford $80+ oil. This created an imbalance between supply and demand. The oil industry is a finely tuned “flow” business with a lot of inertia. A small drop in demand can have a large impact on price because global storage capacity is limited, and because oil producers are motivated to produce at the maximum rate because their capital expenditures are already spent and cash flow can keep them alive for a period, even if they sell at a loss. Similarly, countries like Saudi Arabia are motivated to produce at the maximum possible rate, even if prices are low, because they need the cash to pay for the social services that keep them in power.

- In summary, oil now costs more to produce than consumers can afford. And maybe more than is required for economic growth.

- The first expected outcome is low prices. Check.

- The next expected outcome is a reduction in exploration and production investment. Check.

- The next expected outcome will be oil company bankruptcies and austerity and social unrest in oil producing countries. Starting.

- The next expected outcome will be a decrease in oil production as existing wells deplete and new wells are not brought on line due to a decrease in investment (see above). Coming soon.

- The next expected outcome will be a decrease in global GDP because every product and service we make or use requires energy. As energy declines so must GDP. Due to the inherent instability of high debt levels in a no or low growth environment this step may occur at any time and may actually precede a decline in oil production.

- The next expected outcome may be a deflationary collapse as existing debts can no longer be serviced by a shrinking economy. There is some uncertainty in this step because governments will do everything possible to avoid a collapse and may take extreme measures such as printing and spending money to force inflation. This may work for a while but will end at the same destination by destroying the value of money.

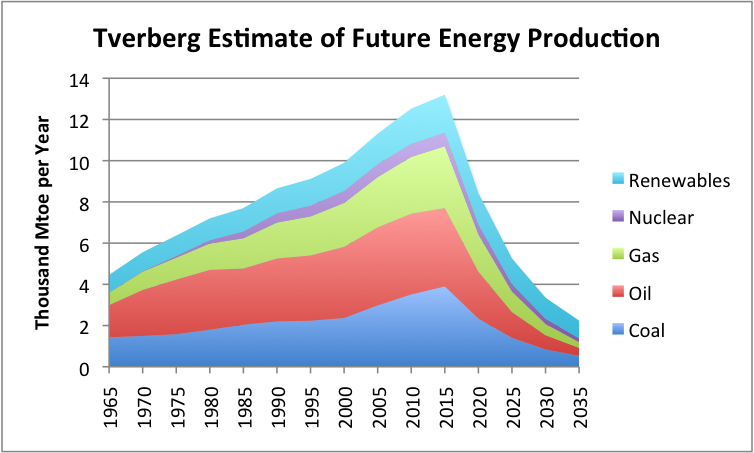

- In the end the world will one way or the other be much poorer. It may be impossible to invest enough to rebuild oil production to the level we enjoy today, and it will certainly be impossible to invest enough to replace oil with renewable energies as they cost more than today’s $80+ oil we already cannot afford.

A caveat. Economic changes rarely move in a straight line. The oil price has oscillated since the 2008 crisis and may do so again. We can be certain however that with each oscillation the oil that is left in the ground will be more expensive to extract and therefore the trend will and must be bad.

So to answer the opening question, the low oil prices we see today are in fact an indicator that peak oil is upon us now.

What should we do?

There are no good solutions. I believe that aggressive conservation policies are needed. And we should do what we can to reduce our debt level through austerity. Conservation and debt reduction will further reduce economic activity and may cause a depression but we might have some ability to control the contraction rather than being forced to surf an uncontrolled crash.

The good news is that most in the developed world can survive with much less than we currently consume. And an economic contraction will be good for climate change.

The bad news is that economic depressions almost always result in war and war this time will only make things worse, even for the victor, because there are no spoils to capture, and war will burn up what’s left even faster.