Another brilliant must read essay by Tim Morgan. There is not one economist in a thousand that understands the relationship between energy and wealth, and yet it’s the most important thing required to understand our economy today.

Think about it. How can it be that well-educated intelligent experts understand everything except obvious facts that imply bad news? Nothing other than inherited denial can explain this powerful and destructive human behavior.

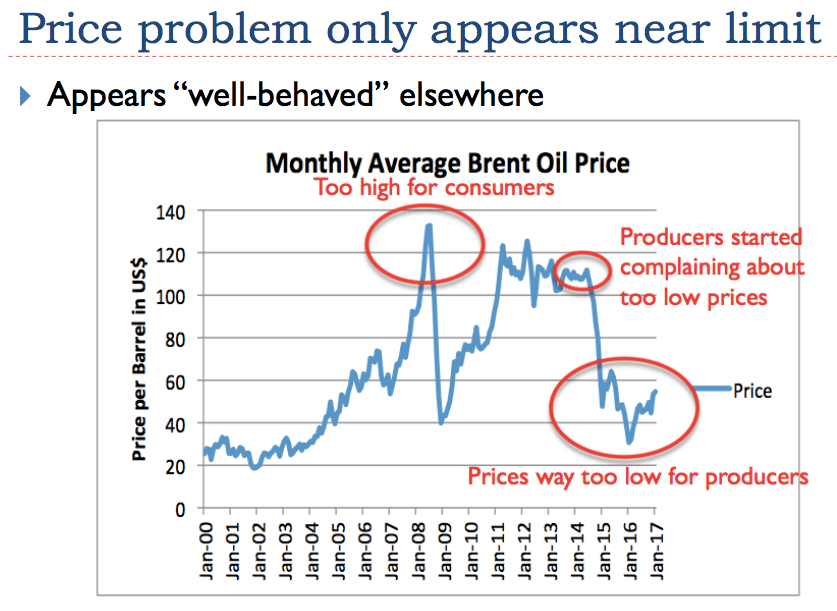

https://surplusenergyeconomics.wordpress.com/2017/02/16/87-a-world-economy-snapshot/

World trend ECoE is estimated at 7.8% in 2015 – up from 6.4% in 2010 – and is projected to rise to 10.0% by 2021. The latter corresponds to an EROEI of just 9:1 which, if you understand EROEI, spells very big trouble. ECoEs are already high enough to help explain why the world economy is now stuck in “secular stagnation”.

ECoE is best understood as an economic rent. It is a “cost”, but not in the conventional sense of that word because, of course, no money actually leaves the system. Rather, a rising ECoE compels us to spend more on energy and, therefore, less on everything else.

This shows up most obviously in household budgets as a rise in the cost of essentials, which leaves the individual or household less to spend on everything else. Again taking Britain as an example, the cost of household essentials rose by 48% between 2006 and 2016, far outstripping much smaller increases in wages (+21%) and general CPI inflation (+25%). At the level of national economies, much the same occurs, with the cost of essentials outpacing both income and broad inflation as ECoE increases.

This is one reason why seemingly-positive data on the economy as a whole increasingly clashes with individual experience – the data says the economy is growing, but the individual feels poorer, not wealthier. An increasing ECoE – and its transmission through the cost of essentials – helps explain this apparent contradiction. As neither conventional economics nor governments understand this mechanism, policymakers find themselves baffled by trends which do not seem to accord with the data available to them.

So global GDP increased by an aggregate of $20.1tn in the ten years culminating in 2015. But, as you will also see, world debt increased by far more – $76.5tn – over the same period. This means that, aggregated over a trailing ten-year (T10Y) period, $3.81 was borrowed for each $1 of reported growth in GDP.

Obviously, this trajectory is not sustainable – over ten years, economic growth of 22% was far exceeded by an increase of 45% in debt. If the projected increase of $23tn in GDP between 2015 and 2021 happens, and is accompanied by borrowing at the same ratio as the T10Y number (of $3.81 per growth dollar), debt would increase by $87tn, or 36%, over that period.

Ominously, the T10Y measure has been rising steadily – back in 2010, the T10Y ratio was only $2.84 of borrowing for each growth dollar. Even at the $3.81 multiple, however, the ratio of world debt-to-GDP would rise from 216% to 244% – and even this number requires acceptance that reported GDP numbers are an accurate reflection of underlying output.

It seems pretty clear that the enormous rate of borrowing in recent years has flattered GDP by creating “growth” that is really no more than the spending of borrowed money. This, of course, brings forward consumption at the cost of increased liabilities in the future.

On this basis, underlying world GDP in 2015 was $95tn, 17% below the reported $114tn. Just as important, trend growth is far lower when measured on an underlying basis, where world economic output is growing at about 1.2% annually.

This figure is nowhere near a consensus in the range 3-4%. That consensus rate of growth may be deliverable – but only if we carry on spending borrowed money.

A world in denial

Logically, the practice of inflating GDP by spending borrowed money cannot continue indefinitely. This is not a “new normal”, but a “new abnormal”. Most obviously, the aggregate amount of debt is rising much more rapidly than economic output, making the debt burden ever harder to support. Since the global financial crisis (GFC) of 2008, the economy has only managed to co-exist with this debt mountain at all thanks to the slashing of interest rates to near-zero levels.

ZIRP (meaning “zero interest rate policy”) has its own costs, some of which are only now gaining recognition. Savers have suffered very seriously from monetary policies designed to keep borrowers afloat, which, perhaps, is why the concept of “moral hazard” seems to have fallen out of the vocabulary. Last summer, after the most recent cut in interest rates, the deficit in British pension funds rose to £945bn, more than 50% of GDP, and evidence of pension value destruction has emerged on a worldwide basis. Ultra-cheap money keeps afloat businesses which in normal times would have gone under, creating space for new, vibrant enterprises – so the necessary process of “creative destruction” has been stymied by monetary manipulation.

In short, we are living in an unsustainable “never-never-land”, in which cheap debt both misrepresents and undermines real economic performance.