Yesterday, the leader of the world’s largest and strongest economy called his central banker a “bonehead” for not lowering interest rates below zero.

Today, the European Central bank (ECB), which according to Trump is not led by a bonehead, reduced interest rates and increased money printing:

The ECB reduced the deposit rate to minus 0.5% from minus 0.4%, and said it’ll buy debt from Nov. 1 at a pace of 20 billion euros ($22 billion) a month for as long as necessary to hit its inflation goal.

Trump and the ECB correctly understand that lower interest rates are required to stimulate growth, and yet rates are already near zero, which suggests real growth is no longer possible.

A non-bonehead would seek to understand the underlying reason growth is constrained. They might begin by reading today’s essay by Gail Tverberg in which she makes 11 important points:

https://ourfiniteworld.com/2019/09/12/our-energy-and-debt-predicament-in-2019/

[1] Our problem is not just that oil prices that are too low. Prices are too low for practically every type of energy producer, and in many parts of the globe.

[2] The general trend in oil prices has been down since 2008. In fact, a similar trend applies for many other fuels.

[3] The situation of prices being too low for many types of energy producers simultaneously is precisely the problem I found back in December 2008 when I wrote the article Impact of the Credit Crisis on the Energy Industry – Where Are We Now?

[4] In the right circumstances, a rapidly growing supply of cheap energy products can help the world economy grow.

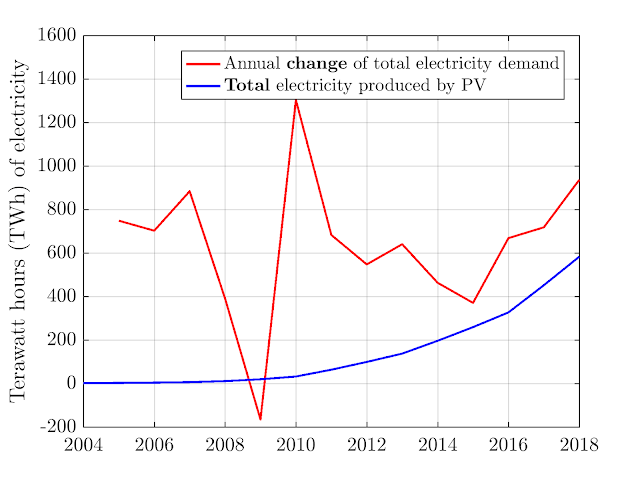

[5] It is striking that the period of rapid energy consumption growth between World War II and 1980 corresponds closely to the long-term rise in US interest rates between the 1940s and 1980 (Figure 6).

[6] Starting about 1980, the US economy began substituting rapidly growing debt for rapidly growing energy supplies. For a while, this substitution seemed to pull the economy forward. Now growth in debt is failing as well.

[7] Since 2001, world economic growth has been pulled forward by China with its growing coal supply and its growing debt. In the future, this stimulus seems likely to disappear.

[8] The world economy needs much more rapidly growing debt if energy prices are to rise to a level that is acceptable to energy producers.

[9] The world economy seems to be running out of truly productive uses for debt. There are investments available, but the rate of return is very low. The lack of investments with adequate return is a significant part of what is preventing the economy from being able to support higher interest rates.

[10] Since 1981, regulators have been able to prop up the economy by reducing interest rates whenever economic growth was faltering. Now we have pretty much run out of this built-in source stimulus.

[11] The total return of the economy seems to be too low now. This seems to be why we have problems of many types, ranging from (a) low interest rates to (b) low profitability for energy producers to (c) too much wage disparity.

Having now learned that economic growth is constrained by the depletion of low cost non-renewable fossil energy, a non-bonehead would then focus on renewable energy to determine what is or is not physically possible, and the implications of trying to substitute fossil with solar and wind energy.

They might begin with this week’s essay by Tim Watkins and would quickly learn that the environmental costs of “green” energy are very high, that “renewable” energy is totally dependent on non-renewable fossil energy, and in any case only produces electricity which does not address the other 80% of fossil energy we depend on.

http://consciousnessofsheep.co.uk/2019/09/09/facing-our-inconvenient-truths/

Having now attained an understanding that there is no possible way to resume economic growth, a non-bonehead would then ask what’s the consequence of attempting to force growth with printed money and negative interest rates? A quick review of history would show there is no free lunch and that monetary shenanigans ultimately destroy currencies which leads to wars and revolutions.

Finally, a non-bonehead would integrate all of the above with an understanding of the ongoing collapse of our planetary ecosystem, including the loss of a climate compatible with civilization. They might begin with this week’s interview with Phillise Todd, who has a good grasp of the big picture, despite her occasional and understandable (as explained by Varki’s MORT theory) lapses into denial.

Understanding now the intractable nature of our predicament, and comparing reality with what our culture believes, a non-bonehead would conclude they are a genetic mutant and that most of our species are boneheads.

When challenged with the criticism that all they do is discuss problems without offering solutions, a non-bonehead would respond with a clear plan:

And the boneheads would ignore it.